How fixed income investors should manage downside risks while targeting high real yields

By Ané Craig, Fund Manager at PSG Asset Management

While 2025 looks set to be quite eventful, the promising news for South African investors is that local fixed income markets seem poised to deliver another year of good real returns. Although we expect investors to benefit from continued positive market dynamics locally, we also anticipate volatile returns over the year given an unpredictable global backdrop and heightened sensitivity to news flow. Risk management will therefore be key – but an over-reliance on volatility indicators in isolation could be misleading.

Last year was a bumper year for bond returns, with the FTSE/JSE All Bond Index (ALBI) delivering 17.3%. With CPI averaging 4.4% for 2024, it means that bond investors saw a 12.9% real return for the year, well in excess of the asset class’s long-term average real return of between 2% and 3% p.a.

Bond markets can be surprisingly volatile

While bonds are considered to be less risky than equities in the long run, this does not mean that they are exempt from volatility in the short term. The CBOE Volatility (VIX) Index is often cited as an important indicator of ‘fear’ (or sentiment) in equity markets. It measures the market’s expected 30-day future volatility by analysing the prices of S&P 500 Index call and put options. Bond markets have their own metric called the Merrill Lynch Option Volatility Estimate (MOVE) Index, and although it is less well-known than the equity market equivalent, it provides an indication of expected volatility in the US bond market. It should be clear that bond markets can be as susceptible to bouts of volatility as equity markets.

Volatility indices: Stocks and bonds

Sources: PSG Asset Management and Bloomberg

For this reason, many income investors equate managing risk within their portfolios with keeping volatility as low as possible. Investors into well-diversified, professionally managed income funds should rightfully expect a smoother return profile than what is available in the bond market itself. However, there are dangers to constructing an investment portfolio with low volatility as the primary goal, or using volatility as the key indicator of risk in a fixed income portfolio.

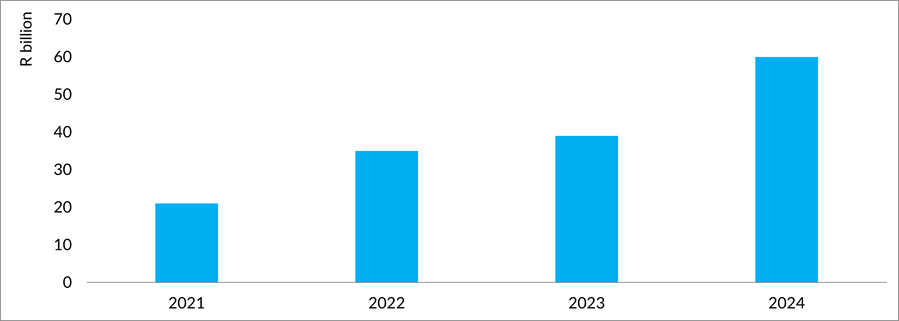

Instruments that don’t mark to market have enjoyed a popularity boom

In recent years, we have seen a rise in the use of instruments that do not mark to market in fixed income portfolios. These include private debt instruments, and credit-linked and structured notes. In many cases, these instruments offer an enticing yield, but undoubtedly a large part of their attraction lies in the ‘less volatile’ return profile they contribute to portfolios. Consequently, credit-linked notes (CLNs) and structured notes have grown in popularity over the last few years, reaching R60bn in issuance in 2024.

JSE-listed credit-linked and structured note issuance

Sources: Standard Bank Research, Bloomberg and JSE

According to our research, more than two-thirds of these instruments have never been re-marked: price changes only reflect periodic coupon payments. This means that the price of these types of instruments can be quite different to the economic reality of the underlying investments.

How valuation perception and reality can diverge when instruments don’t mark to market

In the example below, the Sasol CLN price shows no volatility whereas the underlying valuation changes with fundamental factors and market sentiment. In the case of Sasol, a listed entity, it is possible to observe a market price for the instrument. When the price of Brent crude oil dropped below US$20 per barrel during the pandemic, Sasol’s bonds reflected the market’s concerns while the pricing of the Sasol CLN below remained unchanged. Following a post-pandemic rally, Sasol’s USD bond pricing adjusted again to reflect higher US Treasury yields and Sasol-specific environmental, social and governance (ESG) concerns. Again, the CLN pricing remained unchanged. Interestingly, the JSE does not require banks that issue CLNs and structured notes to mark the instruments to market based on price changes of their underlying components. The banks allow fund managers to choose whether they want instruments to reflect changes in market pricing or not.

Comparing price volatility: Sasol 2028 USD bond vs its listed derivative

Source: Bloomberg. *The JSE-listed CLN was issued on 15 May 2019, matured on 20 June 2024 and referenced Sasol’s 2028 USD bond.

In the case of private (non-listed) credit, it is not possible to objectively monitor the creditworthiness of the issuer, as financial information is not typically publicly available. The decision to revalue an unlisted instrument depends on the fund manager’s valuation policy. Often, investors are only alerted to problems when private companies start to default on obligations. Thus, although these types of instruments may appear less volatile, the approach to pricing them only masks the inherent risks of the asset, whether positive or negative. This makes it harder for investors to assess the true level of risk they are taking in their portfolios.

Managing risk should not eclipse the focus on preserving capital

A key objective for fixed income investors should be to avoid a permanent loss of capital, as doing so helps to secure their ability to generate returns and income on an ongoing basis. While managing the overall client journey and levels of volatility in a fund is important, we do not believe that fund managers should do so at the expense of meeting the capital preservation objective. In our view, an overreliance on instruments that do not mark to market, in pursuit of stable returns holds significant risks for clients. That is why we remain resolutely focused on managing portfolios in line with our proven 3M investment process. We firmly believe that clients should at all times be adequately compensated for the risks they take on, and ensuring this risk is measured appropriately and transparently is key to ensuring optimal long-term client outcomes.

Insurance technology with a difference.

Say goodbye to complex legacy technology, and hello to a different kind of software solution.